kaedeezign

Bakkt Holdings, Inc. (NYSE:BKKT) lately introduced that the acquisition of Apex and new inorganic alternatives could improve income development in 2023 and the approaching years. I additionally suppose that internationalization efforts, purchasers coming from new sectors, and agreements with new giant purchasers might carry substantial internet gross sales development. Sure, I see dangers from the potential failed restructuring efforts executed within the final quarter or regulatory modifications, nevertheless, BKKT does seem undervalued.

Software program Platform For Crypto And Useful Outlook For 2023

Bakkt connects the digital economic system by providing a software program platform for crypto and redeeming loyalty and reward factors which are issued by purchasers to their prospects. The corporate helps purchasers ship new alternatives to their prospects thanks to interactive web experiences or APIs.

Supply: Firm’s Web site

Bakkt believes that the corporate will probably take pleasure in vital momentum development thanks to the expansion of the worldwide crypto market. I imagine that this is among the causes to take a look on the firm’s enterprise mannequin even when the corporate doesn’t ship a major FCF margin proper now. We’re speaking a few market which may be rising at near 27.8% from 2022 to 2030.

The worldwide cryptocurrency trade platform market measurement was valued at USD 30.18 billion in 2021 and is anticipated to develop at a compound annual development price of 27.8% from 2022 to 2030. The rising reputation of digital belongings, equivalent to cryptocurrencies and Non-Fungible Tokens, is anticipated to extend the demand for cryptocurrency trade platforms. Supply: Cryptocurrency Exchange Platform Market Size Report, 2030

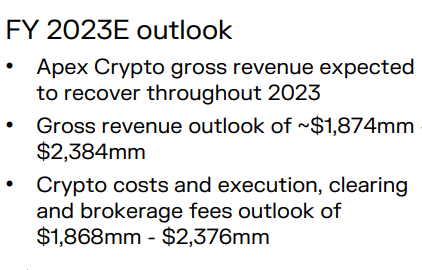

With that concerning the rising market, I imagine that the outlook seems useful. The corporate expects to report gross income near $1.874-2.384 billion, and Apex Crypto sales would recover throughout 2023.

Supply: Quarterly Presentation

Clear Stability Sheet

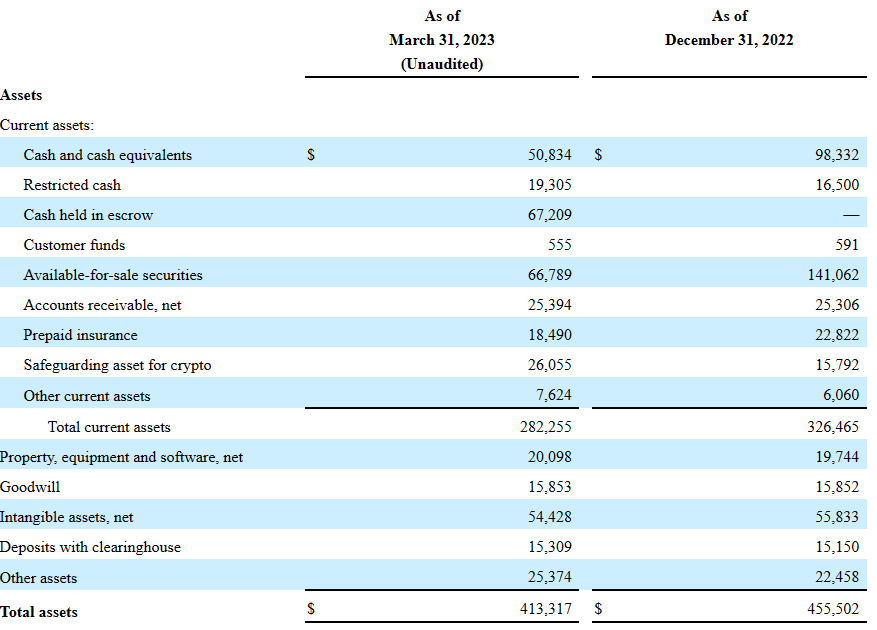

As of March 31, 2023, the corporate reported money and money equivalents value $50 million, with restricted money of $19 million, money held in escrow of $67 million, and accounts receivable of about $25 million.

Additionally, with pay as you go insurance coverage of near $18 million, safeguarding belongings for crypto value $26 million, property, gear, and software program value $20 million, and goodwill of $15 million, whole belongings stand at near $413 million.

The asset/legal responsibility ratio stands at near 4x, and the ratio of present belongings/present liabilities is bigger than 1x. In sum, I believe that the balance sheet appears very solid.

Supply: 10-Q

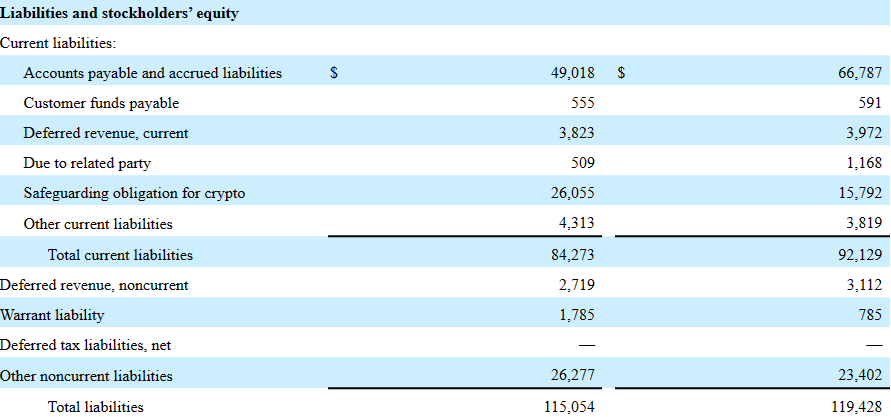

Almost about the overall quantity of liabilities, Bakkt reported accounts payable and accrued liabilities value $49 million, safeguarding obligation for crypto near $26 million, and whole liabilities of $115 million.

Supply: 10-Q

DCF Mannequin: M&A Integration, Worldwide Income, And New Shoppers From New Sectors Would Indicate Vital Upside In The Inventory Value

Beneath my monetary mannequin, I assumed that Bakkt would efficiently develop its crypto platform, and efficiently put money into additional buying and selling capabilities. I additionally imagine that the corporate might broaden its community with new purchasers, which might probably function a income catalyst for the approaching years.

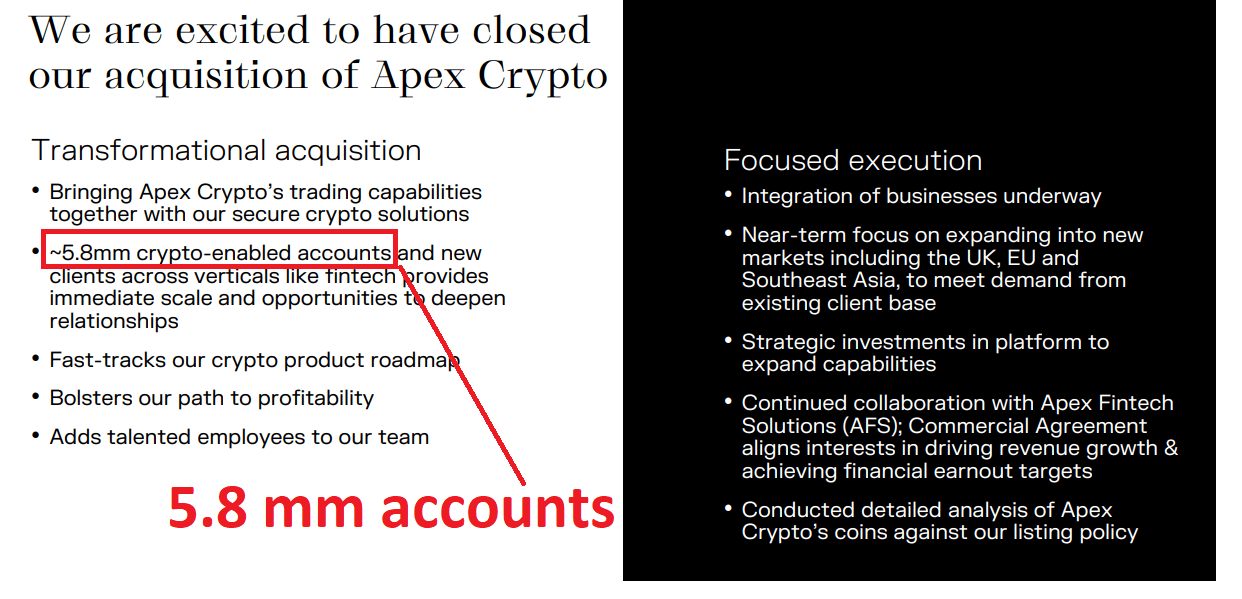

I believe that the mixture of the belongings of Apex could be useful for Bakkt. On this regard, it’s value mentioning that Bakkt is including shut to five.8 million accounts, and can probably improve the FCF margin of the corporate. Administration offered a major variety of particulars concerning the integration with Apex in a latest presentation. I can really feel the optimism from their latest slides.

Supply: Quarterly Presentation

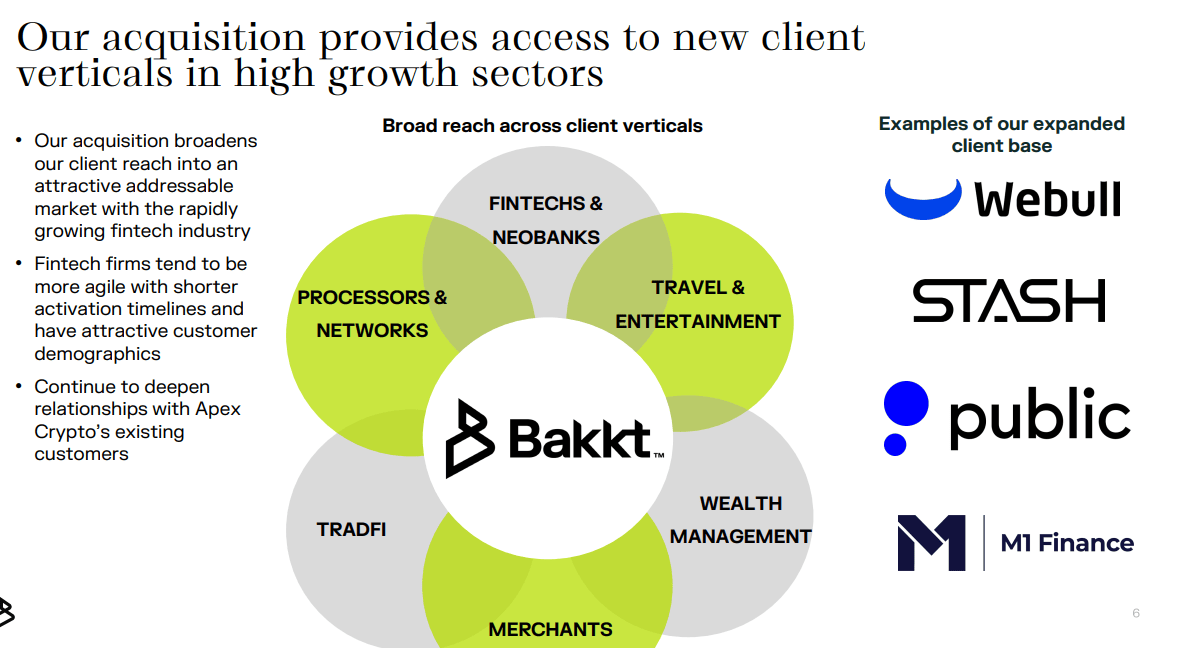

I imagine that essentially the most fascinating factor concerning the acquisition is that Bakkt obtains entry to a major variety of sectors. Many new gamers will probably be capable of strive the platform supplied by Bakkt, which might probably multiply the alternatives for income technology.

Supply: Quarterly Presentation

Additional acquisitions are fairly seemingly primarily as a result of the stability sheet doesn’t present loads of debt, and administration proved that it was able to work inorganically. As well as, Bakkt famous that it’s continually on the lookout for new acquisitions to make income development extra dynamic. I believe that expectations of extra inorganic development could speed up the expectations about future FCF development and internet gross sales development.

We’ll proceed to be opportunistic and consider strategic acquisitions which have compelling advantages for our enterprise. Supply: 10-K.

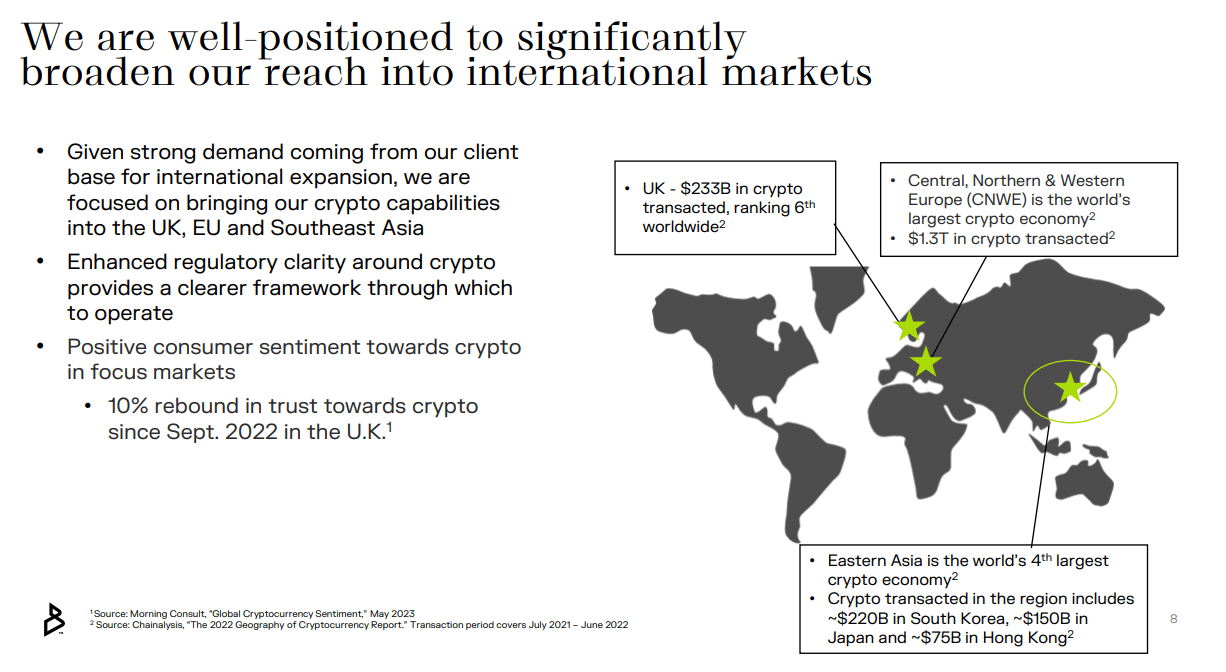

Beneath my DCF mannequin, I might anticipate a rise in worldwide income primarily coming from Asia, Western Europe, and the UK. On this regard, administration famous that there’s robust demand from purchasers everywhere in the world due to new regulatory readability in lots of international locations.

Supply: Quarterly Presentation

Moreover, I might expect additional connections with new giant purchasers. On this regard, it’s value noting that the corporate already works with large firms like MasterCard (MA), Visa (V), International Funds (GPN), Fiserv (FI), and Caesar’s (CZR). For my part, potential giant purchasers will probably be concerned with Bakkt as soon as they see that administration already works with giant and established companions.

We accomplice with main manufacturers and anticipate to develop prospects on our platform by way of these relationships. We’ve already constructed an intensive community of purchasers throughout quite a few industries together with monetary establishments, retailers, and journey and leisure. These purchasers embody MasterCard, Visa, International Funds, Fiserv, and Caesar’s. We imagine that this technique will allow us so as to add transacting accounts and quantity extra rapidly and extra effectively than a direct-to-consumer mannequin, particularly as a comparatively younger firm working in an area like crypto which may be novel to some customers. Supply: 10-k

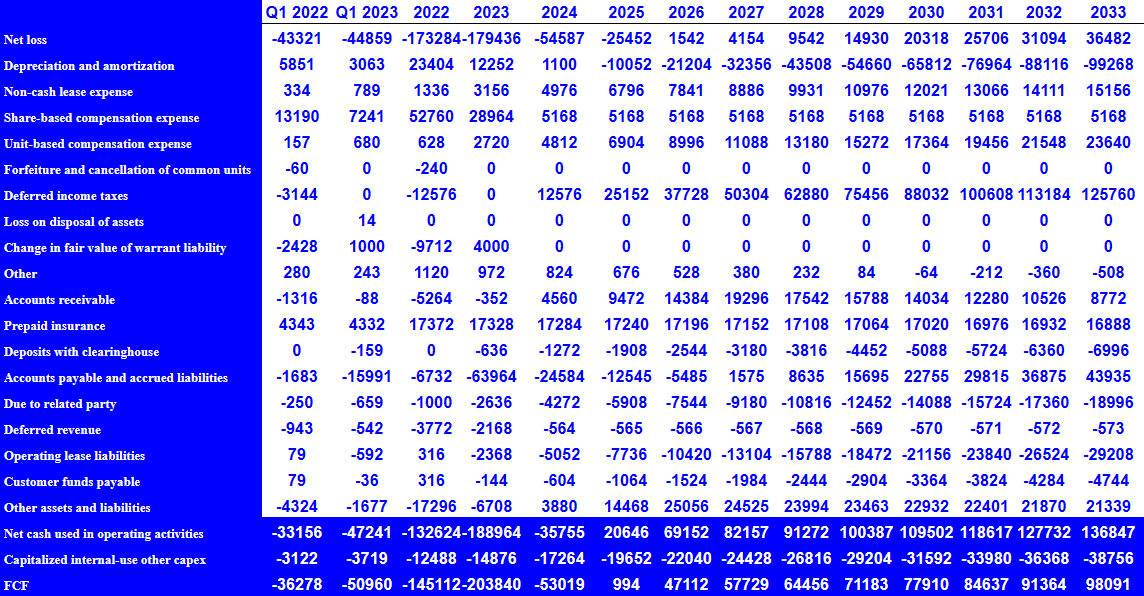

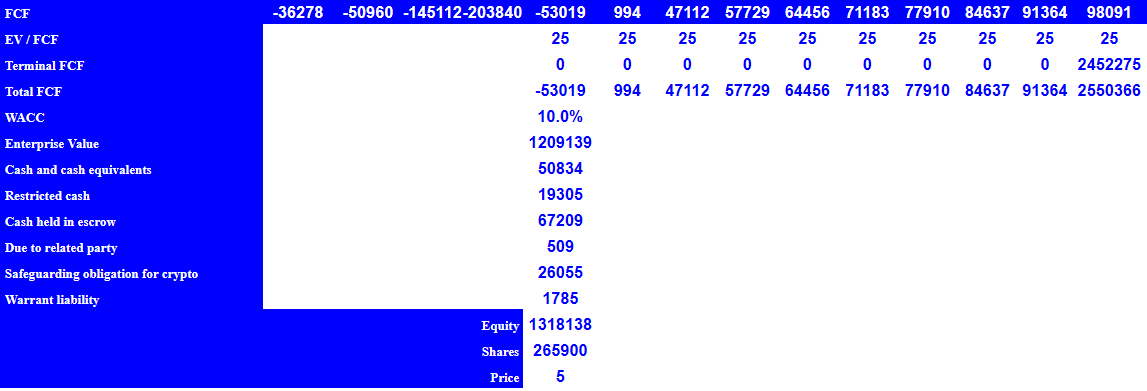

My monetary mannequin contains 2033 internet earnings value $36 million, 2033 depreciation and amortization of -$100 million, share-based compensation expense of near $5 million, unit-based compensation bills of $23 million, and deferred earnings taxes near $125 million.

Additionally, with 2033 modifications in accounts receivable of about $8 million, 2033 pay as you go insurance coverage of near $16 million, modifications in accounts payable and accrued liabilities value $43 million, and modifications in debt resulting from associated events of -$19 million, 2033 internet money utilized in working actions could be about $136 million. Lastly, if we assume 2033 capitalized internal-use different capex of about -$39 million, 2033 FCF could be about $98 million.

Supply: My Monetary Mannequin

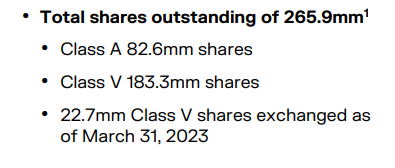

If we assume a terminal EV/FCF of 25x and a reduction near 10%, the implied enterprise worth could be near $1.209 billion. Additionally, including money and money equivalents near $50 million, restricted money of $19 million, and money held in escrow value $67 million, and subtracting safeguarding obligation for crypto value $26 million and warrant legal responsibility of $1 million, the implied fairness valuation could be $1.318 billion, and the truthful worth could be $4.95 per share.

Supply: My Monetary Mannequin

Dangers From Lack Of Buyer Development, And Decrease Transacting In Crypto And Loyalty Factors

Making an allowance for the present state of Bakkt, I imagine that essentially the most worrying threat would come from a scarcity of latest purchasers. In addition to, if the variety of transacting in crypto and loyalty factors executed by every present buyer lowers for no matter purpose, internet gross sales expectations would additionally decline considerably. Because of this, I believe that we might anticipate decrease FCF expectations and decrease implied truthful valuation. Administration offered a full rationalization of those dangers within the final annual report.

If we’re not capable of carry new purchasers onto the platform, a lot of whom pays us subscription charges for our platform companies, our income and enterprise concern may very well be negatively impacted. Moreover, a lot of our future income is dependent upon transaction charges earned from prospects transacting in crypto and loyalty factors and the margin we cost in reference to these transactions. If we’re not capable of proceed to develop our base of purchasers, we won’t be able to proceed to develop our buyer base, our revenues, or our enterprise, which might negatively influence our enterprise, monetary situation, and outcomes of operations and will trigger us to be unable to proceed as a going concern. Supply: 10-k

Bakkt will probably provide new options and new further purposes within the platform. New options is probably not appreciated by purchasers, or regulators could block a few of the new functionalities that the corporate could wish to provide. Lack of latest improvements or failed new options would probably result in decrease FCF development and a decrease implied worth.

We’re working to develop our service choices, together with, for instance providing crypto rewards. Our platform would require further improvement in an effort to add the entire further functionalities and options deliberate by our administration and activate our service choices. There might be no assurance that the extra functionalities and options presently deliberate for our platform might be efficiently developed in a well timed style or in any respect. The addition of functionalities to our platform could require regulatory approvals, could improve our regulatory obligations and the diploma of regulatory scrutiny we face, and will make regulatory compliance extra advanced and burdensome. Supply: 10-k

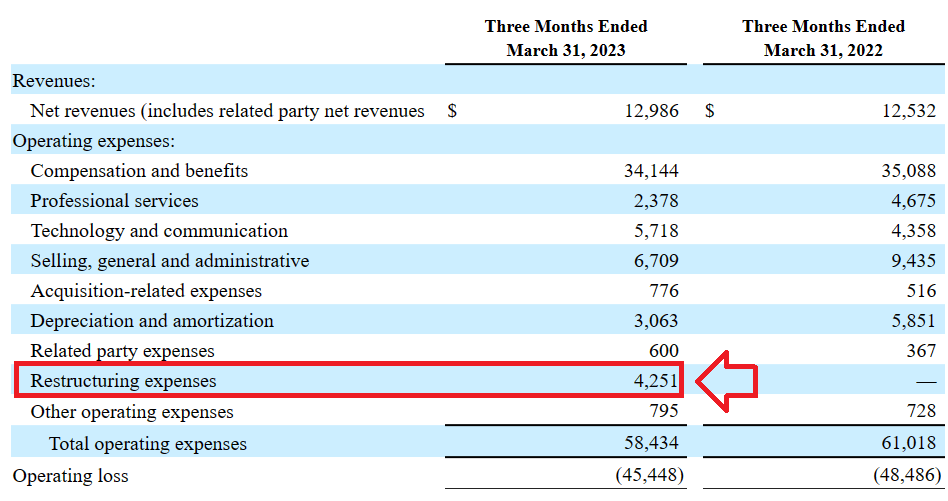

Within the final quarterly report, Bakkt included restructuring bills that I didn’t see within the quarter ended March 31, 2022. Quarterly restructuring stood at $4.2 million. I might be frightened about failed restructuring efforts. If proficient personnel go away the corporate, Bakkt could endure decrease income development within the coming future and even lack of know-how. Probably the most worrying is that traders on the market would probably not know whether or not these initiatives might be profitable.

Supply: 10-Q

The corporate famous that restructuring bills intend to simplify operations, and can deal with scalability and product improvement. For my part, traders will do good by trying fastidiously on the following strains.

Restructuring bills of $4.3 million through the three months ended March 31, 2023, consists of severance prices and accelerated vesting of non-cash compensation as a part of our enterprise simplification initiatives to deal with capabilities with robust product market match and scalability. Supply: 10-Q

Almost about the fairness construction, I don’t like that the corporate got here with completely different share courses, which most traders on the market could not recognize. For my part, it creates loads of points for professionals making calculations concerning the truthful worth. Many traders is probably not concerned with Bakkt due to its fairness construction, which can decrease the demand for the inventory, and have an effect on the price of fairness.

Supply: Quarterly Presentation

Conclusion

Bakkt could profit from the rising cryptocurrency market, and with the acquisition of Apex, administration expects income development to extend in 2023. Moreover, administration seems to be new acquisitions, which can improve future inorganic development. I additionally suppose that additional internationalization, new purchasers from new sectors, and extra options within the platform might speed up natural development from 2023. I do see dangers from failed restructuring efforts, new regulatory modifications, and failed M&A efforts, nevertheless, I imagine that Bakkt seems a bit undervalued.

{kind=link}